Understanding the Different Types of Real Estate Loans: How to Make Informed Decisions

When it comes to purchasing or refinancing a property, navigating the world of real estate loans can be overwhelming. With so many options available, it’s essential to understand the different types of loans, their benefits, and their drawbacks. In this article, we’ll delve into the various types of real estate loans, helping you make informed decisions and achieve your goals.

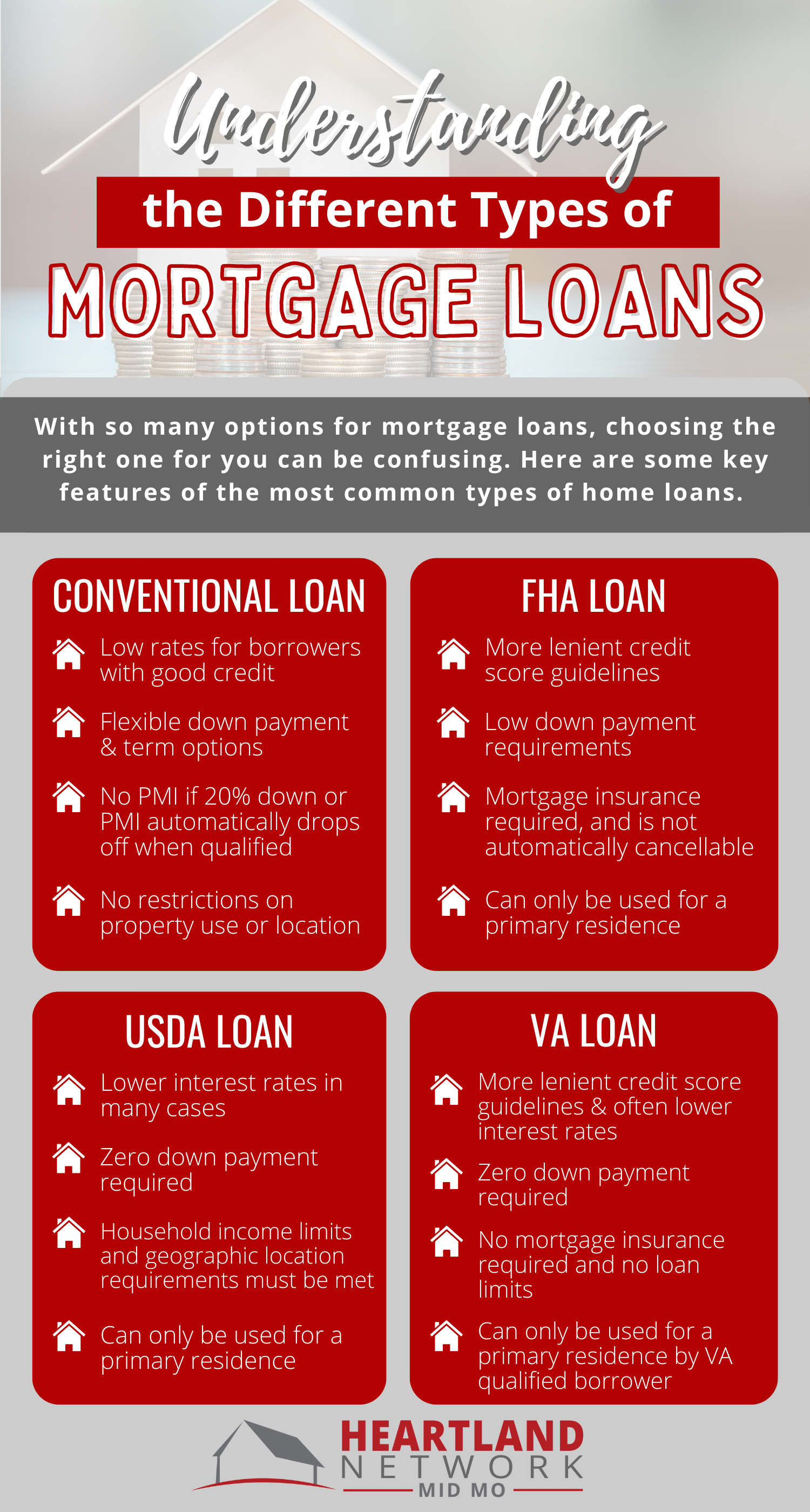

Conventional Loans: The Most Common Choice

Conventional loans are the most popular type of real estate loan, accounting for more than 60% of all mortgages. These loans are offered by private lenders and are not insured or guaranteed by the federal government. Conventional loans typically require a down payment of at least 20% of the purchase price, although some programs may allow for lower down payments. The benefits of conventional loans include:

- Lower mortgage insurance premiums

- Higher loan limits

- Flexibility in repayment terms

However, conventional loans often have stricter credit score requirements, and borrowers may need to pay private mortgage insurance (PMI) if they put down less than 20%.

Government-Backed Loans: A Safer Alternative

Government-backed loans, such as FHA and VA loans, are insured or guaranteed by the federal government. These loans are designed to help low-to-moderate-income borrowers purchase homes, often with lower down payment requirements. Government-backed loans offer:

- Lower down payment requirements (as low as 3.5% for FHA loans)

- Easier credit score requirements

- Lower mortgage insurance premiums

However, government-backed loans may have lower loan limits and stricter appraisal requirements.

Jumbo Loans: For the High-End Buyer

Jumbo loans are designed for buyers who need to finance a more expensive property. These loans exceed the conforming loan limits set by Fannie Mae and Freddie Mac, typically ranging between $510,400 and $765,600. Jumbo loans offer:

- Higher loan limits

- Flexibility in repayment terms

- Competitive interest rates

However, jumbo loans often require higher credit scores, larger down payments, and may have higher interest rates.

Interest-Only Loans: A Short-Term Solution

Interest-only loans allow borrowers to pay only the interest on their loan for a specified period, typically 5-7 years. During this time, the borrower’s monthly payments are lower, as they’re not paying principal. Interest-only loans offer:

- Lower monthly payments